Per Capita GDP of China vs. the United States (Forecast using Japan)

.png)

FAQ

1. Why does it matter if China catches up to the same GDP per capita as the United States?

China, even in 2021, is the largest economy by PPP and is the second-largest by GDP behind the United States. As of 2019, China also had 1.398 billion people compared to the United States, only having 328 million people. So if China reaches the same GDP per capita as the United States, it will be a far larger economy than any other economy in the world.

2. Is Japan a good guide for when China may reach the United States in terms of GDP per capita?

Japan gives some guidance as to what is possible. Japan had 92.5 million people in 1960, while the US had 180.7 million people. So the US was still almost twice as large as Japan. China is over 4x as large as the US currently. So they may face hurdles due to their size. However, their size is also a benefit. Companies worldwide will have a large incentive to obtain access to China's market by giving China the technology it needs to reach the US in terms of GDP per capita.

3. Why has Japan fallen so much in the past 25 years?

In terms of PPP per capita, Japan has continued to grow. In terms of GDP per capita, Japan has not. This disparity is due to the impact of exchange rate fluctuations.

4. Is PPP or GDP a better measure to use?

PPP is a good measure of how well off the people in a country are. However, GDP is good in terms of how much of an impact the country can make globally. For a country to buy or invest in another country, an exchange rate will have to be used.

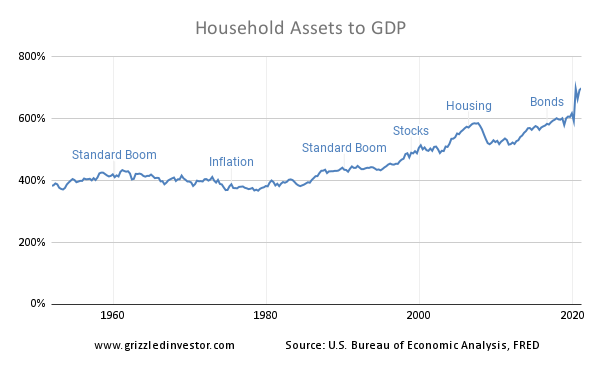

Household Assets to GDP

July 25, 2021 - Assets

FAQ

1. Why do household assets relative to GDP matter?

The wealthier people feel, the more they spend. So if assets are too high relative to income, it is also indicative of assets being expensive. This overvaluation could portend a future period where assets decline relative to GDP. This decline will cause people to increase savings, reducing consumption and GDP growth.

2. What have been the major influences on household assets relative to GDP for the past 60 years?

Leading up to the mid-1960s, there was a standard stock market boom, where stocks went to the high end of their historical valuation range (up until that point). In the 1970s there was increased inflation and rising interest rates. Rising rates helped depress stock and bond prices. Declining inflation and interest rates in the 1980s brought asset prices back up. In the 1990s there was a tremendous increase in stock valuations that peaked in 2000 that increased assets. After the 2000-02 bear market in stocks, there was a tremendous increase in real estate valuations leading up to 2006. The 2008-09 recession coincided with large declines in real estate and stocks. Since that time, high-quality bond yields have fallen so low that they yield negative returns after inflation. These low bond yields are now supporting stock and real estate prices as well.

3. What is likely for asset values going forward?

The low bond yields of today are not permanent. At some point, rates will rise relative to inflation and they will depress asset prices again.

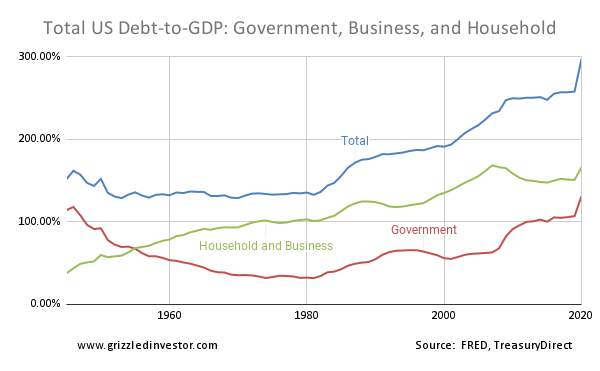

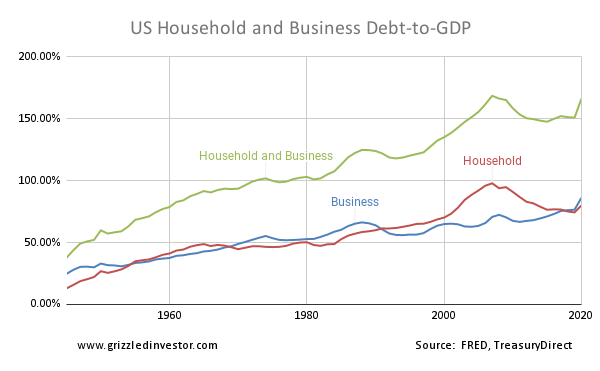

Total United States Debt to GDP - Government, Business, and Household

June 9, 2021 - Debt

FAQ

1. Why does the total debt in an economy matter?

The more debt, the more fragile the economy. Government debt makes it harder for the government to support the economy during recessions. Household debt makes it harder for consumers to keep up spending during recessions. Business debt makes it harder for companies to withstand revenue declines during recessions. The result is that recessions can become more severe as there is less support for the economy.

2. What is the impact of adding debt to the economy?

The more debt that is added stimulates the economy, but then later is a drag on the economy as debt payments have to be made. It can be a further drag if the debt is then paid off.

3. Why not just keep adding debt?

Eventually, the economy will be in such a fragile state that lenders may only lend at very high-interest rates. High rates can make the debt unsupportable and lead to a financial crisis with forced deleveraging.

4. Could a forced deleveraging happen to the US?

With Greece, the money was borrowed in a currency not in control by the government, the Euro. So they had a deflationary forced deleveraging. The US government is borrowing in dollars. So rather than suffer a 1930s style deleveraging, the government has the option of allowing inflation to make the debt smaller by producing more dollars.

5. What do you think will happen?

In the run-up to the housing crisis in 2008, households substantially increased mortgage debt. Since then, the government has stepped in to support the economy. Businesses have also been taking advantage of the low-interest rates by adding debt. This process could probably go on a lot longer. Japan has a government debt to GDP of 255%. The longer it goes on, the more fragile the economy becomes. Once the deflationary pressure of China subsides, and this could still be decades away, interest rates may rise as China buys less US debt to depress its currency. Higher rates could create a deleveraging process that the US government and the Federal Reserve may try to cushion. This cushioning then could lead to sustained high inflation.

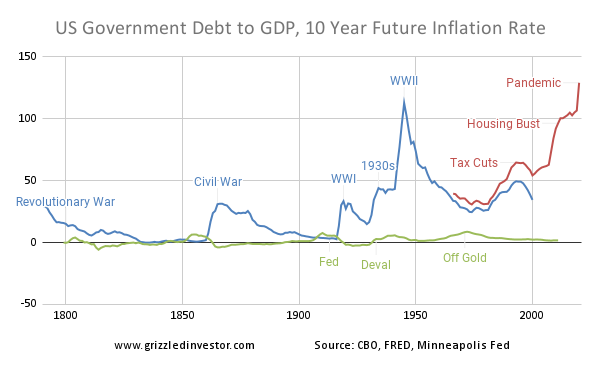

US Government Debt and 10 Year Inflation

May 24, 2021 - Inflation, Debt

FAQ

1. Why is there a red and a blue line?

There is a historical and a current source for the debt-to-GDP data. The blue line represents the historical source, and the red line represents the current source.

2. What is the chart saying?

Prior to the creation of the Federal Reserve and the federal income tax in 1913, exploding deficits were the result of wars. A war created a lot of spending, debt, and inflation, then after a war ended, there was a period of deflation, saving, and reducing debt loads.

Since 1913, this cycle has been broken. The depression in the 1930s led to enormous spending projects to offset declining GDP and deflation. The dollar relative to gold was also devalued, and gold was banned for US citizens. The US was only on a gold standard for international conversion after that point.

This prevented the natural deflation after World War II that would have kept the value of the dollar stable with gold. This increased price level culminated in the US abandoning the US gold standard completely in 1971.

In the 1980s, conservatives decided to cut taxes to prevent ballooning government spending and force spending cuts later. The tax cuts led to budget deficits, which led to an increase in debt. Then the financial crises around the housing bubble in the mid-2000s led to more spending. Finally, the pandemic in 2020 led to even more spending. Debt-to-GDP is now higher than it has even been in the United States. However, it has been higher in other counties before and now.

3. What is the significance of the chart going forward?

The discipline of the country has been lost. The debt level isn't an immediate issue, but if it were to continue to expand or if interest rates were to rise, it could become an issue. Considering the economy may have become accustomed to the stimulus over the past 30 years, there could be a difficult period should than stimulus have to end. Alternatively, the country may face a period of high inflation to bring debt in line.

4. How should someone gaurd against the fallout from this?

It depends on what happens. If there was a deflationary retrenchment, bondholders could do very well. However, if there is an inflationary working off of the excess, then borrowers would benefit. Inflation could help stocks and real estate. However, if real yields return to historical levels, there could be valuation compression for these asset classes that could offset the increased growth rates.

5. What do you think will happen?

I think it will always be easier to have an inflationary response. So that will win out in the short-term to intermediate-term. However, eventually, things may get out of hand enough that the system is radically changed. There could be a return to a gold standard, and it would be a big adjustment, but it may be deemed worth it because the damage from the old policies just got too extreme.

6. Why haven't we hit the point where people want a change in policy?

We did have a significant change in Federal Reserve policy in the late 70s and early 80s, where interest rates increased substantially to combat the most considerable peacetime inflation in US history. Had inflation not subsided so much since then, maybe that would have been enough. One thing that has happened since 1980 is the rise of China. It is a huge deflationary force in the world. It may have helped to contain inflation. Once that deflationary pressure subsides, that is when I would expect more significant inflation, higher interest rates, and the debt level to become a problem.

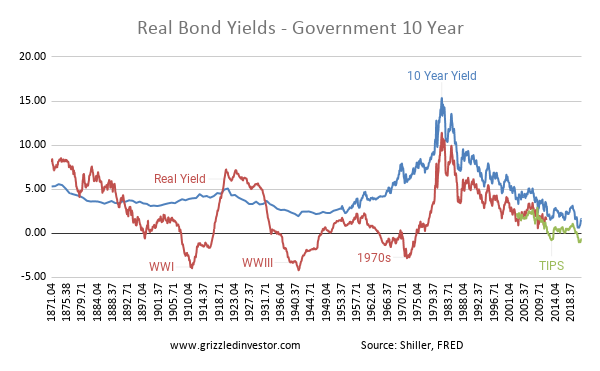

Real Bond Yields - Government 10 Year

May 19, 2021 - Valuation, Bonds

FAQ

1. How is this related to bond valuation?

The premium of bonds over inflation should be stable and positive. However, when investors misread future inflation, the real returns can become negative. This miscalculation happened during World War I (WWI), World War II (WWII), and during the inflation in the 1970s. In recent years the Government 10 Year TIPS are providing a negative real return. Historically this has meant bonds were overvalued. To the extent other assets, such as stocks and real estate, are priced based on bond yields, those assets could suddenly become expensive as well should the bond valuation revert to its historical average.

2. How are TIPS yielding a negative return?

The Federal Reserve is currently purchasing assets. These purchases have the impact of reducing yields and also increasing potential future inflation pressure. Both of these features will suppress the yield on TIPS. Real yields can become much more negative should inflation surge, as has happened during WWI, WWII, and the 1970s. So even at these negative yields, TIPS still offer some inflation protection.

3. What are TIPS?

TIPS stands for Treasury Inflation-Protected Securities. The government is guaranteeing a certain return above inflation. In the current instance, the government is guaranteeing a certain negative return relative to inflation. However, if inflation surges, this return may still do better than standard government bonds that do not have this inflation protection.

4. How is the real return calculated?

The yield on government 10-year bonds minus the actual inflation over the next 10 years provides the real return to bondholders for that specific date.

5. Why do you show the real return series and the TIPS series?

We know the real return for periods further than 10 years back. For more recent periods, we can estimate what the real return will be using TIPS.

Excess CAPE Yield (ECY) and Subsequent 10 Year Annualized Excess Returns

May 17, 2021 - Valuation, Stocks

_and_Subsequent_10_Year_Annualized_Excess_Returns.png)

FAQ

1. What is this chart saying?

The chart says that the stock market's valuation has some impact on returns over many years, in this case, 10 years. Valuation may not matter much at all over a day, week, month, or year. However, over many years there is a mean reversion tendency with the market's valuation that provides some impact on returns. This impact is most notable at the extremes when valuation is extremely cheap and extremely expensive, so the impact of valuation starts to dominate the other forces that govern stock market returns.

2. What isn't valuation perfect?

There is a reason why markets get expensive or cheap in the first place. These causes, while ultimately temporary in the grand scheme of things, can come and go in a way that isn't guaranteed. So valuation gives some edge. Understanding these other trends is needed to improve our understanding of future returns.

3. What is CAPE?

CAPE is the average inflation-adjusted earnings for the past 10 years divided by the inflation-adjusted stock price. This manipulation helps to remove cyclical fluctuations in earnings, which can fall dramatically during recessions.

CAPE was developed by Robert Shiller. You can get more information at Robert Shiller's website.

4. What is the Excess CAPE Yield?

Converting CAPE to a yield allows you to compare it to bond yields. Since stocks are riskier than bonds, we would expect the yield on stocks to be greater than the yield on bonds. If the spread is very high, then stocks may be cheap. If the spread is very narrow, then stocks may be expensive.

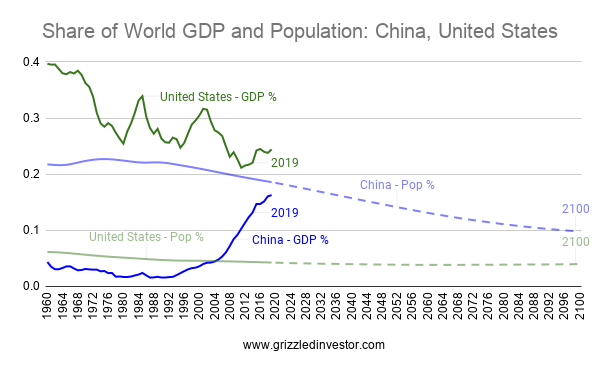

Share of World GDP and Population - China and the United States

May 12, 2021 - China

FAQ

1. Why does China matter?

The United States has been the largest economy in the world for over 100 years. However, China has a much larger population. Since the late 1970s reforms, China has experienced rapid growth. It is now on track to be the largest economy in the world, and by some measures, it already is, such as Purchasing Power Parity. Not only could it become the largest, but it could also dwarf the United State's economy in size. It could even become larger than the economies of Europe and North America combined. However, China faces a population growth decline that should limit its relative size by 2100. So its potential dominance isn't as great as it currently seems.

2. Where is China's share of world GDP headed?

The per capita income of China is still far below the United States. So there is a lot of room for growth. However, the population advantage is shrinking. So instead of becoming 50-60% of the world economy, China may only get to 30-40%. Instead of the US falling to 12-13% of world GDP, the US may only fall to 15-16%.

3. What is GDP?

Gross Domestic Product (GDP) was first developed in the 1930s to understand the Great Depression. It measures the production in an economy. The bigger the GDP, the more a country can produce. The value of production is also equal to the income of the economy.

4. What reforms did China undergo in the late 1970s?

Mao Zedong ruled the communist People's Republic of China from when it was founded in 1949 until his death in 1976. His death then created an opening for alternative economic models to take root. The communist system in China did not lead to the economic gains that more capitalist systems could achieve in that period. So the new economic reforms borrowed from capitalist principles. The impact was small in relative terms compared to the world, but as China has grown, China's impact on the world economy has grown.

5. Why is China's population growth falling?

From 1979–2015, China had a "one-child policy" where families were only allowed to have one child, although up to 50% of the population may have been able to have up to two children. China's population is expected to peak in 2031 at almost 1.5 billion and fall to under 1.1 billion by 2100. In that same period, the US population is expected to grow from 351 million to 434 million.

6. What are the population percentage lines after 2019?

Those are estimates based on projections from the United Nations and can be found at Macrotrends.

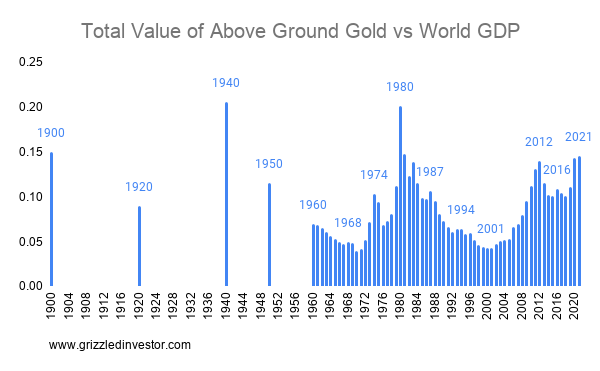

Gold Valuation - Total Value of Above Ground Gold vs World GDP

FAQ

1. Why is gold compared to World GDP a measure of gold valuation?

Since gold has been used as a currency, it makes sense to compare its value to all the transactions that take place in an economy in a year, which GDP provides one measure of.

2. What is the point of going back to 1900?

In the late 1800s and early 1900s, much of Europe and the United States were on gold standards. That period would serve as a benchmark for the value of gold if the world returned to a gold standard.

3. What is a gold standard?

A gold standard is when a country's currency is measured in terms of gold. A country will typically hold gold. A country will then be willing to buy and sell gold in exchange for its currency at a fixed price.

4. Why was the gold standard abandoned?

There was a massive deflation in the early 1930s that led to significant unemployment throughout the 1930s until World War II. The thinking is that the gold standard in the US prevented the Federal Reserve from stimulating enough during the 1930s. The countries that devalued their currencies relative to gold in the 1930s tended to rebound quicker. That is evidence that policy was too tight in the 1930s. By the 1970s, the price level had risen substantially in the US, but the price of gold in dollars was unchanged since the 1930s. This gap in pricing allowed other foreign governments (US citizens were banned from holding gold from 1933 until 1975) to exchange dollars for gold at extremely favorable prices. Instead of adjusting the price of gold higher, the US abandoned the gold standard entirely.

5. Will we ever get back on the gold standard?

When the colonies started the American Revolutionary War with Great Britain, they issued the Continental currency. Within a few years is lost 99% of its value. When the United States was formed, it then required all money to be backed by gold and silver. So currencies have gone without gold backing before. Currencies have been depreciated into worthlessness before. People have lost faith in currencies before. So we can't rule out similar things happening in the future, but we can't rule out a currency being trusted for a while, either. So it is about keeping an eye on what is happening and trying to pick up any warning signs.

6. Hasn't the dollar already lost a lot of value?

Sure, it has. In terms of dollars, from 1900 to 1967, gold went from $20.67 to $35 an ounce. Since 1967 gold has gone to over $1700 an ounce. It didn't even double after 67 years, and since then, it has gone up over 40x. However, on a year-to-year basis it hasn't been losing value, in terms of inflation, anything like past hyperinflationary periods. So year to year, it has been tolerable enough for most of the people in the United States that it hasn't created the political will for change.

7. Why hasn't measured inflation, such as the CPI, been even worse?

This is a good question, maybe the question of our time. One thing that has happened since 1980 is the rise of countries like China. China likely has contributed to price pressure for inputs, such as commodities. However, for finished goods, the massive influx of cheap labor may have been keeping inflation down in the developed world. However, once Chinese wages become more in line with the most developed countries, the deflationary pressure it brings may likely come to an end. That is when I would expect sustained inflationary pressure to emerge.

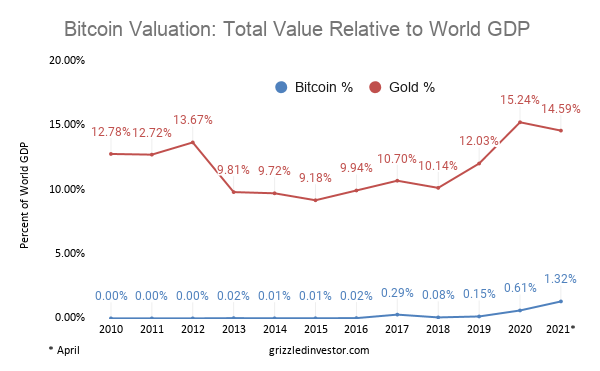

Bitcoin Valuation - Total Value Relative to World GDP

April 27, 2021 - Bitcoin, Gold, Valuation

FAQ

1. What is valuation?

Valuation gives some benchmark to know whether an asset is undervalued, fairly valued, or overvalued.

2. Why use gold as a benchmark?

For Bitcoin to have value, it needs to be used as a currency. Gold is a commodity that has been used as a currency in the past. Central banks still hold gold as a form of reserves. The amount of gold relative to world GDP serves as one benchmark for the value bitcoin needs to have to be used as a currency for the world.

3. We used gold as a currency?

On August 15, 1971, the US stopped being willing to convert dollars to gold. Before that, the US had a Gold Standard, where the US dollar was backed by gold. If the US printed too much money, dollars could be converted to gold at a fixed price. In 1971 that price was $35. Gold in recent years has traded above $1000.

4. What if Bitcoin isn't adopted throughout the entire world?

To the extent Bitcoin becomes a niche currency, it should be expected to attain some fraction of the target gold valuation. Currently, it is priced at about 10% of gold's valuation. That could translate to 10% of the currency used worldwide.

5. What if gold is undervalued as a potential worldwide benchmark?

Gold's undervaluation would mean bitcoin's potential is even greater.

6. What about silver and other cryptocurrencies?

Silver has been used as a currency in the past. Silver has also been used with gold in various forms of bimetallism in the 1800s in the United States. So it is conceivable other cryptocurrencies could be used in conjunction with bitcoin. An expanded analysis that includes silver and other cryptocurrencies has some merit.

7. Will bitcoin become a major currency?

Seemingly unusual things have been used as currency in the past. Salt was used as a currency in China. Cowry shells are still used as currency on the Papua New Guinea island of East New Britain.

Currencies come and go throughout history. The fiat Continental Congress currency used during the American Revolutionary War fell by 99% within a few years and was replaced with the US dollar. It was one reason the US dollar was backed by gold in the first place.

So the limited amount of Bitcoin combined with people being interested in using it as a currency means it could have a role as a currency. As far as becoming a major currency, it is hard to imagine the world transacting in bitcoin overnight.

In time, it may evolve into a major currency. There could be tremendous volatility along the way, as there has been in the past. If it becomes a major currency, it has a huge upside, but if it is abandoned in the future in favor of something else, it could become essentially worthless.