Real Bond Yields - Government 10 Year

May 19, 2021 - Valuation, Bonds

FAQ

1. How is this related to bond valuation?

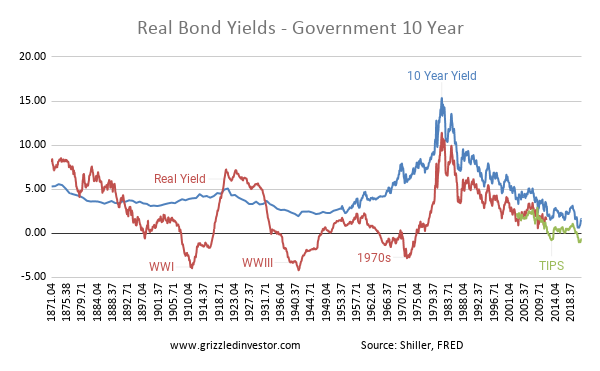

The premium of bonds over inflation should be stable and positive. However, when investors misread future inflation, the real returns can become negative. This miscalculation happened during World War I (WWI), World War II (WWII), and during the inflation in the 1970s. In recent years the Government 10 Year TIPS are providing a negative real return. Historically this has meant bonds were overvalued. To the extent other assets, such as stocks and real estate, are priced based on bond yields, those assets could suddenly become expensive as well should the bond valuation revert to its historical average.

2. How are TIPS yielding a negative return?

The Federal Reserve is currently purchasing assets. These purchases have the impact of reducing yields and also increasing potential future inflation pressure. Both of these features will suppress the yield on TIPS. Real yields can become much more negative should inflation surge, as has happened during WWI, WWII, and the 1970s. So even at these negative yields, TIPS still offer some inflation protection.

3. What are TIPS?

TIPS stands for Treasury Inflation-Protected Securities. The government is guaranteeing a certain return above inflation. In the current instance, the government is guaranteeing a certain negative return relative to inflation. However, if inflation surges, this return may still do better than standard government bonds that do not have this inflation protection.

4. How is the real return calculated?

The yield on government 10-year bonds minus the actual inflation over the next 10 years provides the real return to bondholders for that specific date.

5. Why do you show the real return series and the TIPS series?

We know the real return for periods further than 10 years back. For more recent periods, we can estimate what the real return will be using TIPS.