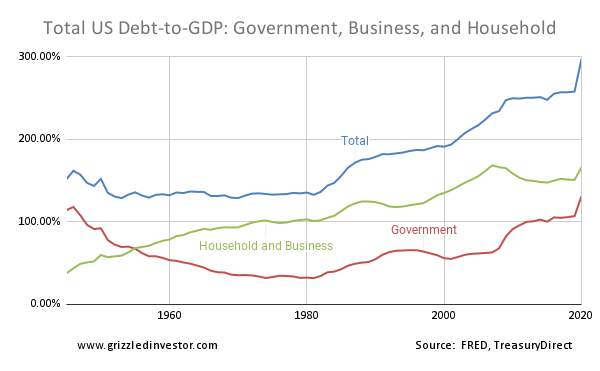

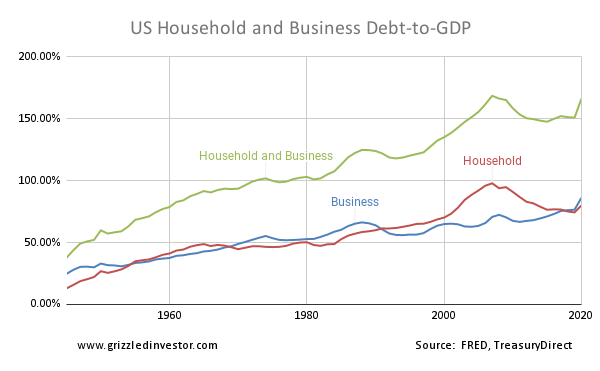

Total United States Debt to GDP - Government, Business, and Household

June 9, 2021 - Debt

FAQ

1. Why does the total debt in an economy matter?

The more debt, the more fragile the economy. Government debt makes it harder for the government to support the economy during recessions. Household debt makes it harder for consumers to keep up spending during recessions. Business debt makes it harder for companies to withstand revenue declines during recessions. The result is that recessions can become more severe as there is less support for the economy.

2. What is the impact of adding debt to the economy?

The more debt that is added stimulates the economy, but then later is a drag on the economy as debt payments have to be made. It can be a further drag if the debt is then paid off.

3. Why not just keep adding debt?

Eventually, the economy will be in such a fragile state that lenders may only lend at very high-interest rates. High rates can make the debt unsupportable and lead to a financial crisis with forced deleveraging.

4. Could a forced deleveraging happen to the US?

With Greece, the money was borrowed in a currency not in control by the government, the Euro. So they had a deflationary forced deleveraging. The US government is borrowing in dollars. So rather than suffer a 1930s style deleveraging, the government has the option of allowing inflation to make the debt smaller by producing more dollars.

5. What do you think will happen?

In the run-up to the housing crisis in 2008, households substantially increased mortgage debt. Since then, the government has stepped in to support the economy. Businesses have also been taking advantage of the low-interest rates by adding debt. This process could probably go on a lot longer. Japan has a government debt to GDP of 255%. The longer it goes on, the more fragile the economy becomes. Once the deflationary pressure of China subsides, and this could still be decades away, interest rates may rise as China buys less US debt to depress its currency. Higher rates could create a deleveraging process that the US government and the Federal Reserve may try to cushion. This cushioning then could lead to sustained high inflation.

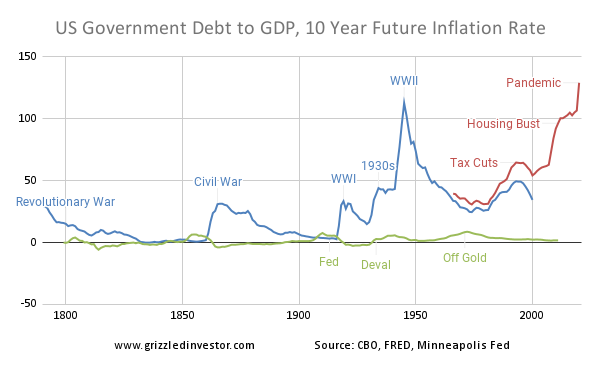

US Government Debt and 10 Year Inflation

May 24, 2021 - Inflation, Debt

FAQ

1. Why is there a red and a blue line?

There is a historical and a current source for the debt-to-GDP data. The blue line represents the historical source, and the red line represents the current source.

2. What is the chart saying?

Prior to the creation of the Federal Reserve and the federal income tax in 1913, exploding deficits were the result of wars. A war created a lot of spending, debt, and inflation, then after a war ended, there was a period of deflation, saving, and reducing debt loads.

Since 1913, this cycle has been broken. The depression in the 1930s led to enormous spending projects to offset declining GDP and deflation. The dollar relative to gold was also devalued, and gold was banned for US citizens. The US was only on a gold standard for international conversion after that point.

This prevented the natural deflation after World War II that would have kept the value of the dollar stable with gold. This increased price level culminated in the US abandoning the US gold standard completely in 1971.

In the 1980s, conservatives decided to cut taxes to prevent ballooning government spending and force spending cuts later. The tax cuts led to budget deficits, which led to an increase in debt. Then the financial crises around the housing bubble in the mid-2000s led to more spending. Finally, the pandemic in 2020 led to even more spending. Debt-to-GDP is now higher than it has even been in the United States. However, it has been higher in other counties before and now.

3. What is the significance of the chart going forward?

The discipline of the country has been lost. The debt level isn't an immediate issue, but if it were to continue to expand or if interest rates were to rise, it could become an issue. Considering the economy may have become accustomed to the stimulus over the past 30 years, there could be a difficult period should than stimulus have to end. Alternatively, the country may face a period of high inflation to bring debt in line.

4. How should someone gaurd against the fallout from this?

It depends on what happens. If there was a deflationary retrenchment, bondholders could do very well. However, if there is an inflationary working off of the excess, then borrowers would benefit. Inflation could help stocks and real estate. However, if real yields return to historical levels, there could be valuation compression for these asset classes that could offset the increased growth rates.

5. What do you think will happen?

I think it will always be easier to have an inflationary response. So that will win out in the short-term to intermediate-term. However, eventually, things may get out of hand enough that the system is radically changed. There could be a return to a gold standard, and it would be a big adjustment, but it may be deemed worth it because the damage from the old policies just got too extreme.

6. Why haven't we hit the point where people want a change in policy?

We did have a significant change in Federal Reserve policy in the late 70s and early 80s, where interest rates increased substantially to combat the most considerable peacetime inflation in US history. Had inflation not subsided so much since then, maybe that would have been enough. One thing that has happened since 1980 is the rise of China. It is a huge deflationary force in the world. It may have helped to contain inflation. Once that deflationary pressure subsides, that is when I would expect more significant inflation, higher interest rates, and the debt level to become a problem.